More Blogs

May 3, 2026

The average Canadian homebuyer pays over $20,000 in unnecessary fees during their purchase journey. Every dollar you keep is another dollar toward your children’s education, renovations, or simply building wealth. The key is knowing exactly where your money goes and what you can control.

This step-by-step checklist shows you what to look for when buying a home in Canada, from closing costs and property taxes to inspection red flags and zoning rules. You’ll learn to spot hidden fees, verify true property conditions, and navigate provincial requirements with confidence. ComFree believes you deserve transparency and control throughout your real estate journey, not complicated processes that drain your equity.

Ready to take charge of your next purchase? ComFree provides the educational resources and tools you need to buy and sell with confidence while keeping thousands in your pocket.

This comprehensive 25-point home buying checklist Canada follows a logical sequence that protects your interests at every step. Start with your finances—secure pre-approval and map out your complete budget before you get emotionally attached to a property. Then move through neighbourhood research, property evaluation, and due diligence before making an offer. Each section builds on the previous one, giving you the financial clarity and risk awareness needed to make confident decisions and avoid costly surprises.

Provincial rules vary significantly across Canada, so bookmark sections that apply to your location. Use this checklist as your conversation guide when meeting with mortgage brokers, home inspectors, and real estate lawyers. Ask direct questions, request written explanations, and don’t move forward until you understand each step. You’re in charge of this process—this checklist keeps you organized and ensures nothing important gets overlooked while you maintain control of your equity.

Before you start shopping for homes, know exactly what you can afford. A mortgage pre-approval gives you a firm spending limit and protects you from rate increases while you shop. This isn’t just a ballpark figure — it’s your financial foundation for confident decision-making.

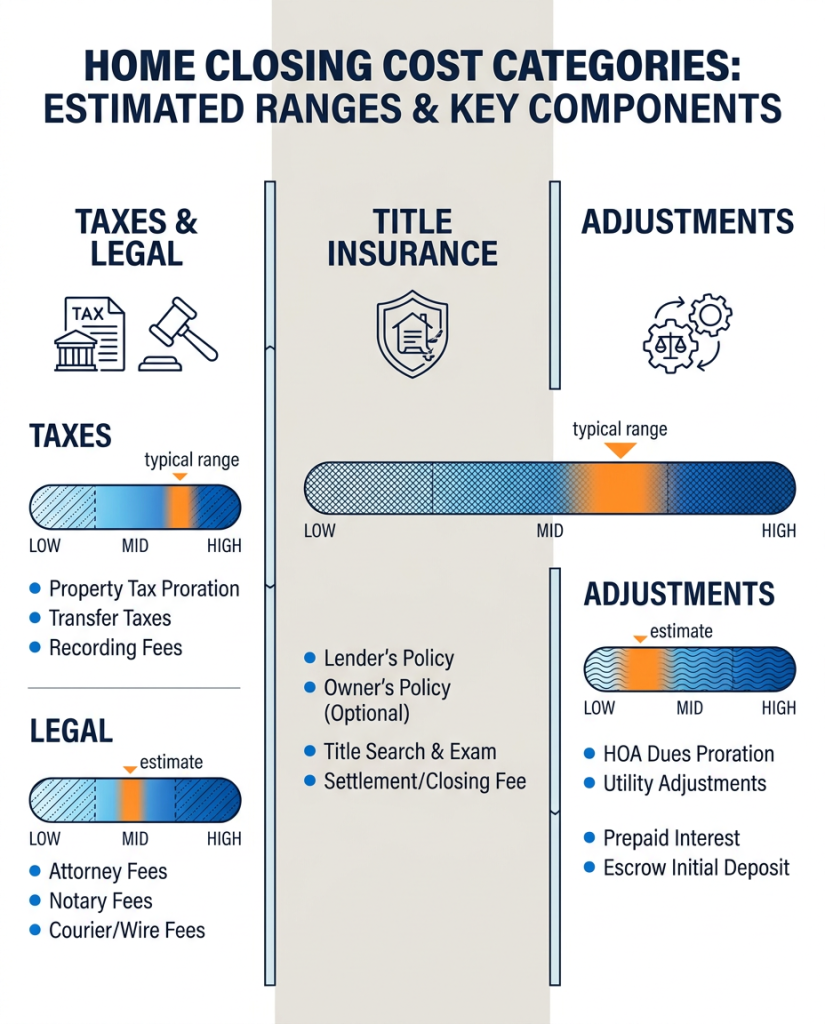

Understanding closing costs in Canada means planning for 2% to 5% of your purchase price on top of your down payment. Land transfer tax typically represents the largest chunk, ranging from 0.5% to 2.5% depending on your province and municipality. For example, Ontario’s land transfer tax can reach 2.5% in Toronto, while Alberta charges a flat $50 registration fee. Legal fees run $1,500 to $3,000, while title insurance costs $300 to $600 to protect against ownership disputes. Property tax adjustments, utility connections, and home inspection fees add another $1,000 to $2,500 to your closing costs.

Before finalizing your budget, research first-time buyer rebates that can save thousands of dollars. Many provinces offer land transfer tax refunds — Ontario provides up to $4,000 for eligible first-time buyers. Create a line-item spreadsheet with every expected cost, then add a 10% buffer for unexpected expenses like expedited document processing or additional title searches. Remember to include moving costs, utility deposits, and immediate home setup expenses in your total budget — these often surprise new homeowners and can easily add $3,000 to $5,000 to your first month.

Property taxes become your second-largest housing expense after your mortgage payment. Unlike your mortgage, these payments never end and tend to climb each year. You can take control by researching the real tax burden before you fall in love with a property.

Understanding all costs upfront puts you in control of your purchase decision and helps you avoid surprises that traditional agents might gloss over.

Your neighbourhood research in Canada starts with your own observations, not online listings. Walk the streets during morning rush hour, school pickup time, and weekend evenings to understand real noise levels and traffic flow. Check street lighting after dark and note how safe you feel walking alone. Listen for train horns, highway hum, or construction sounds that might not show up in a quick afternoon visit. These details affect your daily comfort and future resale appeal.

Beyond what you can see and hear, municipal planning websites reveal the bigger picture that can significantly impact your investment. Search your city’s planning portal for proposed developments, road widenings, and transit expansions that could boost or hurt property values. Check local bylaws about parking restrictions, short-term rental rules, and noise ordinances that impact your lifestyle. Compare crime statistics through your provincial police service website and explore community centres, libraries, and parks that add real value to family life. This research takes a few hours but protects years of equity.

Your daily routine shapes your quality of life more than any fancy feature. Smart buyers test real-world logistics before signing, because commute time and transit access in Canada can make or break your budget and sanity.

School catchment boundaries can impact your property value by 5–15% compared to similar homes in different districts, so verify them directly with the school board rather than trusting online maps. A home two streets over might feed into a completely different school, affecting both your children’s education and your resale potential. Contact schools to confirm enrolment capacity and ask about any boundary reviews planned for the next five years that could change your assigned school.

Beyond schools themselves, family-friendly amenities within walking distance make daily life smoother and improve your daily experience as a homeowner. Map out distances to parks, libraries, community centres, and childcare options using actual walking routes, not straight-line measurements. Check municipal recreation programs, youth sports leagues, and after-school care availability through your local municipality’s website. These school districts and amenities create the foundation for family life and often determine which neighbourhoods maintain strong demand from other parents when you’re ready to sell.

Informed buyers research beyond first impressions to uncover factors that affect daily comfort and long-term value. This neighbourhood safety and development research gives you concrete information to guide your offer strategy and avoid costly surprises.

Your property choice should match your maintenance capacity and family needs, not just your budget. Detached homes offer privacy and control but typically require 4–6 hours of weekend maintenance monthly, plus snow removal and exterior repairs. Condos minimize hands-on work but add monthly fees and shared decision-making through condo boards. When comparing detached vs townhouse vs condo options in Canada, consider how much time you realistically want to spend on upkeep versus family activities and career growth.

Multi-level layouts can create challenges as your family evolves, affecting both daily life and future resale appeal. Stairs become obstacles for toddlers learning to walk and aging parents visiting for extended stays. Townhomes often provide the right balance between space and affordability, but shared walls can transmit noise from neighbours’ late-night activities or early morning routines. Limited yard space may also restrict children’s outdoor play or pet ownership — factors that matter more as kids grow and influence buyer interest when you’re ready to sell.

Condos come with shared ownership benefits and restrictions that directly impact your monthly costs and daily freedom. Before you commit to a unit, examine the building’s financial health and governance rules to protect yourself from unexpected fees and lifestyle limitations.

Smart home layout and functionality consistently outperforms impressive square footage when it comes to daily living satisfaction. A well-designed 1,200-square-foot home with built-in storage, wide hallways, and open sightlines often feels larger than a poorly planned 1,500-square-foot space filled with awkward corners and wasted corridors. Look for homes where every room serves a clear purpose and storage solutions are built into the design rather than afterthoughts — this approach maximizes both comfort and resale value.

Measure what matters before you fall in love with a space. Bring a tape measure and check that your dining table fits the designated area, your couch clears doorways, and bedroom furniture leaves walking space. Pay attention to stroller-friendly entries, especially in Canadian winters when you’re juggling boots, coats, and gear. South or west-facing windows deliver natural light that reduces electricity costs and creates warmth during long winter months, making smaller spaces feel bright and welcoming year-round.

Understanding home age and structure in Canada means looking beyond surface appeal to uncover the real costs ahead. While older homes often offer unique character and established neighbourhoods, they can also hide expensive surprises that newer builds simply don’t have. Smart buyers learn to spot the difference between charming vintage details and costly structural headaches.

A professional home inspection protects your investment and gives you negotiating power. Choose a certified inspector who provides a detailed written report with photos and estimated repair timelines. Your Canadian home inspection checklist should cover foundation integrity, roof condition, attic insulation levels, moisture readings throughout the home, electrical systems, plumbing functionality, and HVAC performance. Don’t accept verbal summaries or rushed walkthroughs — you need documentation to make informed decisions and protect yourself legally.

Transform inspection findings into real savings through strategic negotiation. Use repair estimates to request price reductions or seller credits rather than hoping issues will resolve themselves. A $3,000 furnace replacement or $8,000 roof repair becomes leverage for a lower purchase price or cash back at closing. Smart buyers view inspections as fact-finding missions that either confirm their offer price or create opportunities to adjust terms in their favour.

Energy costs add up fast in Canadian winters. Smart buyers look beyond granite countertops to features that actually reduce monthly bills and qualify for government rebates.

Certain materials can trigger red flags with insurers and lenders during your plumbing, electrical, and HVAC inspection. Poly-B plumbing (found in roughly 700,000 Canadian homes built 1978–1995) and aluminum wiring often require updates or specialized coverage that increases costs. Ask about electrical panel age and capacity — panels over 25 years old may need upgrades to handle modern appliances. Ask your insurer to confirm coverage in writing before finalizing your offer, as some companies refuse policies on homes with these materials.

Test every system during your visit to avoid expensive surprises after closing. Run taps in each room to check water pressure and temperature consistency — weak flow or temperature swings signal plumbing issues that can cost $3,000–$8,000 to repair. Ask for furnace service records and confirm heat reaches every room evenly. Check for sump pumps and backflow preventers in basements, especially in flood-prone areas. Document any concerns with photos and get repair estimates to use in negotiations or budget planning.

Legal documents might seem overwhelming, but these records protect your biggest investment and future plans. Proper zoning and permit due diligence in Canada can save you from expensive issues and unlock hidden value potential.

Take control by reviewing your municipality’s flood maps and asking about the property’s sewer backup history. Many Canadian homes face overland flooding or basement water issues during heavy rains or spring melt. Request details about any past claims and verify that your insurance policy includes sewer backup and overland water coverage. These add-ons cost relatively little but can save you thousands if water damage occurs, and some insurers offer discounts for homes with sump pumps or backflow preventers.

Beyond water damage, properties in flood and wildfire risk zones across Canada require additional scrutiny of defensible space and roofing materials. Look for fire-resistant siding, metal or tile roofing, and clear zones around the structure free of combustible vegetation — particularly important in regions like the BC Interior or Alberta’s foothills. In colder climates, test for radon gas, which can accumulate in basements and pose long-term health risks. Professional radon testing costs under $200, and mitigation systems typically run $1,500 to $3,000 — a small investment for peace of mind and future resale confidence.

Smart buyers think like future sellers from day one. When you choose a property with strong future resale value factors, you protect your equity and give yourself more options down the road. The homes that sell fastest and for top dollar share common characteristics that appeal to the broadest range of buyers, and the equity you preserve by avoiding unnecessary commissions can fund improvements that boost these very factors.

Smart buyers in Canada use three main offer conditions: financing approval, home inspection, and status certificate review for condos. These conditions give you legal exits if problems surface, but they’re not meant to be escape hatches for second thoughts. Set realistic timelines that match your lender’s approval process and inspector availability. Five business days work for most inspections, while financing conditions need 10–15 days depending on your lender’s workload and documentation requirements.

When facing multiple offers, resist the urge to waive conditions entirely. Instead, strengthen your offer through a larger deposit, flexible closing dates, or shorter condition periods. You can also include a pre-inspection report or pre-approval letter to show serious intent. Remember that sellers value certainty over small price differences. A clean Canadian home offer with reasonable conditions often beats a higher-priced offer with lengthy or unusual terms that could jeopardize the closing process and cost both parties thousands in legal fees.

Your financing approval is just the first step. The appraisal process Canadian lenders require can still create unexpected challenges, and timing coordination becomes your lifeline to closing day. Stay ahead of these moving parts to protect your purchase.

Start shopping for home insurance quotes at least two weeks before your closing date, not the day before possession. Some property features like oil tanks, wood stoves, or older electrical systems can limit which insurers will cover your home or increase your premiums significantly. Getting quotes early gives you time to address any coverage gaps or factor higher premiums into your budget. Home insurance requirements in Canada vary by province and lender, but most require coverage equal to your mortgage amount plus liability protection.

Beyond basic coverage, add sewer backup and overland water coverage if your area faces flooding risks, but read the fine print on deductibles and coverage limits. Wind and hail damage deductibles can range from $500 to $5,000, depending on your region and roof age. Bundle your home and auto insurance with the same provider to unlock discounts of 10–25% on both policies. Confirm your coverage starts on possession day, not closing day, to avoid any gaps that could leave you financially exposed during your move.

Choosing between a brand new home and an existing property affects your budget, timeline, and daily life in different ways. Both paths have merit, but understanding the real costs helps you pick what works for your family’s situation.

If you’re planning to sell your current home while buying, factor in timing coordination and potential bridge financing needs for either option.

Traditional real estate transactions often bury costs in complex fee structures that buyers never see directly. Ask your representative to disclose all referral fees, kickbacks, and splits tied to your purchase. Many buyers don’t realize they’re indirectly paying both the buyer’s and seller’s agent fees through higher home prices that include these costs. Avoiding hidden real estate commissions starts with demanding transparency about who gets paid what from your transaction.

Flat-fee platforms offer upfront pricing that puts thousands back in your pocket instead of traditional agent charges. On a typical $500,000 home purchase, Canadian buyers can save over $20,000 by choosing transparent alternatives over conventional fee structures. Redirect that money to fund your children’s education, home improvements, or mortgage prepayments that build equity faster. When you control the process and eliminate unnecessary middleman costs, every dollar saved works directly for your family’s future goals.

Smart buyers using effective home negotiation tactics in Canada know that price is just one piece of the puzzle. When you understand what sellers really value, you can create win-win deals that preserve more of your equity while reducing move-in costs.

Take control of your moving timeline by securing bridge financing and possession date coordination in Canada before you need it. Bridge loans typically cost 1–2% above prime but give you 30–120 days to close on your new home while marketing your current one strategically. Most lenders approve bridge financing within 5–7 business days when you have 20%+ equity, eliminating the stress of juggling temporary housing or rushed sale decisions.

Master your closing coordination by starting your moving timeline planning 25 days before possession. Lock in exact handover times for both properties, transfer utilities 48 hours early, and book moving services when rates are lowest. Professional movers, cleaners, and locksmiths offer 10–15% discounts for advance bookings, and you secure your preferred dates. This proactive approach keeps you in the driver’s seat while others scramble with last-minute arrangements and premium pricing.

Poor organization during home buying can cost you thousands in missed opportunities, voided conditions, or last-minute scrambling fees. A solid home buying documents checklist that Canadian buyers can rely on keeps you in control of timelines, protects your investment, and prevents expensive mistakes that derail your purchase.

Buying your first home brings up plenty of questions that deserve straight answers. These responses cut through industry jargon to give you the facts you need to make confident decisions and protect your investment.

Most pre-approvals last 90–120 days, with your interest rate held for that period. Some lenders offer shorter holds or extensions based on market conditions. Start your search immediately after approval to maximize your rate protection and avoid reapplying.

Closing costs range from 2–5% of purchase price, varying by province due to land transfer tax differences. Legal fees, home inspection, and mortgage insurance premiums are generally not tax-deductible. Only moving expenses may qualify if relocating for work.

Never waive inspection unless you’re prepared to cover unexpected repair expenses. Instead, shorten the inspection period to 3–5 business days or offer a higher deposit to strengthen your position. Your financial security matters more than winning at any cost.

Healthy reserve funds — equivalent to 25–50% of the building’s annual operating budget — indicate good financial management and reduce special assessment risk. Recent or planned assessments can signal deferred maintenance issues. Review the last 5 years of financial statements before offering.

Bridge financing lets you buy before selling, using your current home’s equity as collateral. Terms typically last 6–12 months with higher interest rates than regular mortgages. This prevents rushed sales but requires qualifying for both mortgage payments temporarily.

Yes, commission-free platforms like ComFree let you access MLS® listings while keeping more equity in your pocket. You save thousands typically paid to buyer agents while maintaining full control over your decisions and timeline. Transparency beats hidden fees every time.

This buy-a-home-in-Canada checklist gives you the knowledge to make confident decisions from pre-approval to possession. You now understand true costs, know what to inspect, and can spot red flags before they become expensive surprises.

Your next move is simple: leverage tools that keep your hard-earned equity in your pocket. When you’re ready to sell and buy, transparent pricing beats hidden commissions every time. Start planning your move with confidence and clarity — explore ComFree for commission-free support that has helped over 16,000 Canadians save an average of $20,000+ per transaction.

With ComFree, it’s easy! Finally, a platform that connects buyers and sellers. Offering support and service every step of the way, we save you money and give you back control.

These forms are provided to ComFree’s Unrepresented Sellers as a part of their Mere Posting ComFree Listing Contract.

I acknowledge I can only access these forms as a ComFree customer under contract.

These forms are provided to ComFree’s Unrepresented Sellers as a part of their Mere Posting ComFree Listing Contract and in partnership with Zubic Law.

I acknowledge I can only access these forms as a ComFree customer under contract.

These forms are provided to ComFree’s Unrepresented Sellers as part of their Mere Posting ComFree Listing Contract and in partnership with Imperium LLP – Rocky Kim.

I acknowledge I can only access these forms as a ComFree customer under contract.

1. Purchase Your Package

2. We Ship Your ‘For Sale’ Sign

3. Book Your VR Tour

4. Complete Listing Input Forms

5. We Make Your Listing Live

6. Get Support 7 Days a Week

7. iSOLD!