More Blogs

May 3, 2026

The Canadian housing landscape evolved significantly in 2026, with new FHSA contribution limits, updated mortgage qualification rules, and changing provincial incentives. Many first-time buyers feel overwhelmed by these changes, but smart preparation turns uncertainty into opportunity. You can navigate this market confidently when you understand the new rules.

Here’s how to turn that complexity into clarity: This roadmap breaks down how to buy a home in Canada as a first-time buyer 2026 with precision and control. You’ll discover a step-by-step timeline, documents checklist, incentives comparison table, transparent closing costs breakdown, and winning offer tactics that protect your equity. Whether you’re planning to sell your current home, or buy your first, ComFree provides the educational resources and support to keep thousands in unnecessary fees in your pocket throughout your entire real estate journey.

The Canadian housing market in 2026 presents both opportunities and challenges for first-time buyers that require smart preparation. Interest rates have stabilized compared to recent volatility, but regional inventory imbalances and updated lending rules mean you need a clear strategy. Understanding these market conditions helps you budget realistically and negotiate from a position of strength.

Housing supply remains uneven across Canada, with some markets seeing balanced conditions (roughly equal buyers and sellers) while others still favour sellers with limited options. Research recent sales data in your target neighbourhoods rather than relying on list prices alone. Set a firm budget ceiling before you start shopping to avoid emotional overspending when competing offers emerge. Local market knowledge beats national headlines when making purchase decisions.

Understanding mortgage qualification becomes even more important when inventory is tight. Lenders qualify you using the higher of your contract rate plus 2% or the benchmark rate, regardless of your actual mortgage terms. Secure a rate hold early in your search process, typically lasting 90 to 120 days. Think of your 94-day hold as a countdown timer keeping your search focused and protecting against rate increases. This qualification buffer means your approved amount might feel conservative, but it prevents payment shock.

The foreign buyer ban remains in effect through 2026, though exemptions exist for permanent residents and specific circumstances. Municipal short-term rental restrictions also affect investment potential in many cities. Verify current rules in your target area before factoring rental income into your purchase decision. These regulations can impact resale value and financing options, so understand them upfront rather than discovering limitations later.

Buying your first home doesn’t have to feel overwhelming when you follow a proven sequence. The steps to buying a home in Canada in 2026 remain consistent, but timing and preparation matter more than ever. You’ll move through seven distinct phases, each building on the last to keep you organized and confident throughout the process.

Your home buying journey follows this clear path: budget planning, mortgage pre-approval, activating available incentives, property search, making an offer, completing conditions, and closing day. Each step builds on the previous one to protect you from costly mistakes.

Start with budget planning to understand your true buying power, then secure your pre-approval before exploring available incentives. Once your financing foundation is solid, begin your property search with clear parameters. When you find the right home, craft a competitive offer backed by smart conditions, complete your inspections and final checks, then proceed to closing.

With your framework in place, secure a rate hold from your lender as soon as you’re pre-approved. Most lenders offer 90 to 120-day holds, giving you a countdown timer for your search. Use recent sold data from the past 60 to 90 days to guide your offers, not inflated list prices. Set a realistic search radius and stick to it. Chasing properties outside your target area often leads to budget creep and longer commutes.

Align your pre-approval expiry with your planned search timeline. If your hold expires in 94 days, plan to complete your search within 80 days to allow for negotiations. When making offers, prepare for a 5 to 10 business day conditional period for inspections and final financing approval. Book your home inspector and lawyer early so they’re available when you need them. Smart timing prevents rushed decisions and gives you negotiating power throughout the process.

These three steps must happen in sequence because each one builds on the last. Your budget determines your pre-approval amount, and your pre-approval timing dictates when you can activate government incentives for maximum impact.

You’re moving from preparation to action — the exciting part of actually finding and securing your home. Making an offer on a home in Canada in 2026 requires strategy and timing, but with the right approach, you can navigate each step with confidence.

Your down payment strategy in 2026 determines both your upfront costs and monthly payments, directly impacting how much equity you keep in your pocket. Three key factors shape your buying power: tiered down payment minimums, the stress test qualification process, and mortgage insurance costs. Understanding these rules helps you plan confidently and avoid stretching your budget beyond what feels comfortable.

Canada’s tiered system makes homeownership accessible at different price points. For homes under $500,000, you need just 5% down. Between $500,000 and $999,999, you pay 5% on the first $500,000 plus 10% on the remaining amount. A $750,000 home requires $25,000 (5% of $500k) plus $25,000 (10% of $250k) for a total of $50,000. Properties $1 million and above require 20% down, reflecting the government’s focus on supporting first-time buyers in more affordable ranges.

Lenders test your ability to handle rate increases by qualifying you at the higher of your contract rate plus 2% or the current benchmark rate. This stress test protects you from overextending, but it also means your comfortable monthly payment should feel manageable rather than maxed out. If you’re approved for $500,000, consider shopping in the $400,000–$450,000 range to maintain breathing room and preserve more of your savings for other goals.

When you put down less than 20%, mortgage default insurance becomes part of your total cost. Premiums range from 0.6% to 4.5% of your mortgage amount — the less you put down, the higher the premium. A 5% down payment costs 4% in insurance premiums, while 15% down drops that to 2.4%. These premiums get added to your mortgage balance, so factor them into your total purchase budget when calculating your true monthly costs and long-term equity position.

Getting your documents organized before you start the mortgage pre-approval process as a first-time buyer in Canada will speed up your timeline and show lenders you’re serious. Having everything ready means you can move fast when you find the right home — just like having the right preparation helps when you’re ready to sell and move up.

Canada’s 2026 government programs for first-time home buyers offer multiple ways to reduce your upfront costs and boost your buying power. You can stack these programs to potentially access over $100,000 in down payment assistance while reducing your tax burden.

| Program | Benefit | 2026 Limits/Details | Eligibility |

|---|---|---|---|

| First Home Savings Account (FHSA) | Tax-deductible contributions + tax-free withdrawals | $8,000 annual contribution, $40,000 lifetime max | First-time buyers who are Canadian residents aged 18+ |

| Home Buyers’ Plan (HBP) | Withdraw from RRSP tax-free | Up to $35,000 per person ($70,000 per couple) | First-time buyers, 15-year repayment period |

| Ontario Land Transfer Tax Rebate | Refund of the provincial LTT | Up to $4,000 maximum rebate | First-time buyers purchasing in Ontario |

| Toronto Land Transfer Tax Rebate | Refund of the municipal LTT | Up to $4,475 maximum rebate | First-time buyers purchasing in Toronto |

| GST/HST New Housing Rebate | Partial refund on new construction | Up to $6,300 (GST) + provincial HST rebates (homes under $450,000; partial rebate to $550,000) | New homes under $450,000 (partial rebate to $550,000) |

| Provincial Programs | Varies by province | Down payment loans, tax credits, rebates | Check specific provincial requirements |

You can combine an FHSA for tax-deductible savings with HBP withdrawals from existing RRSPs, potentially giving couples access to over $100,000 in down payment funds while minimizing tax impact. Always verify current 2026 thresholds and application deadlines with official government sources before your closing date.

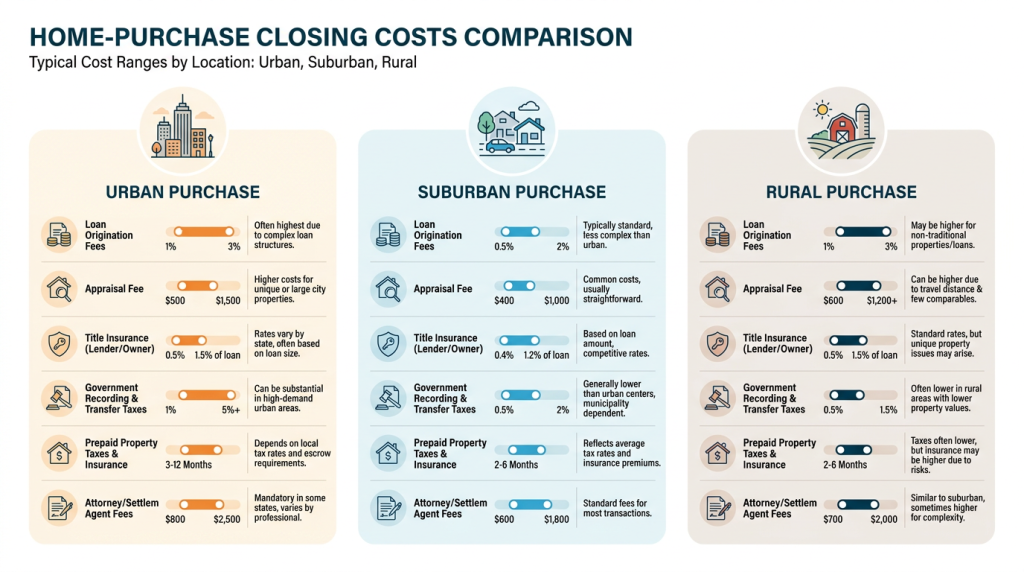

Your down payment is just the beginning, but you can take control by planning for the hidden costs of buying a home in Canada that many first-time buyers don’t anticipate. Understanding these expenses upfront means no surprises and a smoother path to your keys.

| Cost Category | Typical Range | When It Applies | Notes |

|---|---|---|---|

| Legal Fees | $1,200 – $2,500 | All purchases | Includes title search, document prep, registration |

| Land Transfer Tax | 0.5% – 2.5% of purchase price | All purchases | Varies by province; Toronto adds 2.5% municipal tax |

| Title Insurance | $250 – $500 | All purchases | Protects against title defects and survey issues |

| Home Inspection | $400 – $800 | Most purchases | Higher for larger homes or specialized systems |

| Appraisal Fee | $300 – $500 | High-ratio mortgages | Required when down payment is under 20% |

| Property Tax Adjustments | Varies | All purchases | Reimburse seller for prepaid taxes |

| Utility Adjustments | $100 – $400 | All purchases | Oil, water, hydro adjustments to closing date |

| Status Certificate | $100 – $200 | Condos only | Review condo corporation finances and bylaws |

| Septic/Well Inspection | $300 – $800 | Rural properties | Required for properties with private systems |

| Moving Costs | $500 – $2,000 | All purchases | Professional movers or truck rental |

| Total Estimated Range | 1.5% – 3% of purchase price | All purchases | Beyond your down payment |

Create a closing cost checklist 60 days before your target closing date to avoid last-minute surprises. Remember that land transfer tax rates vary significantly across provinces, with some like Alberta charging a flat fee while others like Ontario use percentage-based calculations. Understanding these hidden costs of buying a home in Canada as a first-time buyer means you can budget accurately and move forward with confidence.

Buying a house in Canada without paying realtor commissions starts with understanding that you have more control than the industry wants you to believe. The traditional model assumes you need full-service representation on both sides, but smart buyers are discovering they can protect their savings while still getting expert guidance where it matters most.

In most transactions, sellers pay cooperating commissions of around 4% to buyer agents. When you self-represent, you can often negotiate these savings back through purchase price reductions or closing cost credits. For example, on a $600,000 home, that’s potentially $24,000 in negotiating power. Sellers using commission-free platforms are already saving thousands and may be more flexible on price since they’re not locked into traditional fee structures.

Self-representation requires standardized provincial forms (like OREA agreements in Ontario or BCREA contracts in BC) and clear timelines for all conditions. Your lawyer, home inspector, and mortgage lender become your technical safety net, handling legal and financial verification while you control negotiations. Keep detailed records of all communications, ensure deposits go into proper trust accounts, and know what you can handle yourself — and where to invest in expert guidance.

The smartest approach combines commission-free selling with strategic purchasing, keeping more of your family’s money working for you instead of paying unnecessary fees. When you sell without agent commissions using ComFree’s comprehensive support system, you can afford to be more competitive as a buyer or simply keep more cash for your next down payment. This dual approach works particularly well when timing your sale and purchase together, giving you maximum flexibility and financial control throughout both transactions.

When you know how to make a competitive offer on a home in Canada in 2026, you can win without overpaying in today’s selective market. With inventory remaining tight in many regions and sellers becoming more discerning about buyer qualifications, your offer strength comes from demonstrating certainty rather than just offering the highest price.

Buying your first home brings up plenty of questions, and you deserve straightforward answers. These responses cut through the complexity and give you the confidence to move forward with your purchase plan.

Start with budgeting and mortgage pre-approval, then activate your first-time buyer programs. Search within your approved range, make competitive offers with smart conditions, and plan your closing timeline. The entire process typically takes 60–90 days from pre-approval to keys in hand.

You need 5% down on homes under $500,000, and 5% on the first $500,000 plus 10% on the remainder for homes up to $999,999. CMHC insurance protects lenders when you put down less than 20%, with premiums ranging from 0.6% to 4.5% of your mortgage amount.

Yes, you can stack the First Home Savings Account (up to $8,000 annual contributions in 2026) with the Home Buyers’ Plan for maximum tax advantages. Add provincial land transfer tax rebates and GST/HST new housing rebates where eligible. This combination can boost your buying power by thousands of dollars.

Most pre-approvals include a 90–120 day rate hold, protecting you from rate increases during your search. Get pre-approved before you start looking actively, and treat the expiry date like a countdown to keep your search focused and timely.

In most transactions, sellers pay cooperating commissions from their proceeds, so you typically don’t pay buyer agent fees directly. However, you can self-represent to negotiate credits or fee reductions. ComFree’s educational resources help you navigate this process while keeping more equity in your pocket.

You now have a complete first-time home buyer guide for Canada in 2026. With your budget set, pre-approval secured, and government programs lined up, you’re ready to buy with confidence. No more guessing or second-guessing your next move.

Here’s the game-changer: when you control both your purchase and future sale, you keep thousands more in your pocket. Skip unnecessary commissions during your transaction and that money stays with your family. Smart buyers in 2026 think beyond just getting the keys.

Ready to maximize your savings on both sides? Get started with ComFree for expert guides and seller tools that put you in control of your entire real estate journey.

With ComFree, it’s easy! Finally, a platform that connects buyers and sellers. Offering support and service every step of the way, we save you money and give you back control.

These forms are provided to ComFree’s Unrepresented Sellers as a part of their Mere Posting ComFree Listing Contract.

I acknowledge I can only access these forms as a ComFree customer under contract.

These forms are provided to ComFree’s Unrepresented Sellers as a part of their Mere Posting ComFree Listing Contract and in partnership with Zubic Law.

I acknowledge I can only access these forms as a ComFree customer under contract.

These forms are provided to ComFree’s Unrepresented Sellers as part of their Mere Posting ComFree Listing Contract and in partnership with Imperium LLP – Rocky Kim.

I acknowledge I can only access these forms as a ComFree customer under contract.

1. Purchase Your Package

2. We Ship Your ‘For Sale’ Sign

3. Book Your VR Tour

4. Complete Listing Input Forms

5. We Make Your Listing Live

6. Get Support 7 Days a Week

7. iSOLD!